supermoney

Your money stress, solved by AI.

SuperMoney Has Been Around Since 2013. The AI Layer Might Be What Finally Makes It Matter.

The Macro: Everyone Is Drowning in Financial Advice and Somehow Still Broke

Here’s the thing about personal finance apps: there are approximately one million of them, and most people still have no idea what to do with their money. Mint ran for over a decade and got shut down. YNAB has a passionate cult following and is still confusing to onboard. Rocket Money is fine. They’re all fine. The problem isn’t that people lack access to their transaction data. The problem is that nobody tells them what to do next.

The fintech funding picture is actually interesting right now. Global fintech investment hit $116 billion in 2025, up from $95.5 billion in 2024, according to KPMG. That’s a real rebound after a rough correction period. The WEF’s 2025 fintech report shows revenue growth exceeding industry averages across most verticals. The money is coming back in, and a lot of it is chasing AI-native products that can do something more than surface a pie chart of your spending.

The AI personal finance angle specifically is crowded with early-stage stuff. You’ve got point solutions for budgeting, debt payoff calculators, credit score trackers. What’s actually hard to build is a product that connects all of those things into one prioritized action feed without feeling like it’s upselling you into a loan every thirty seconds. (Spoiler: that tension is very real in this category.)

Where SuperMoney sits is interesting. It was originally a financial services comparison platform, the kind of site you’d land on from a Google search when shopping for a personal loan. The pivot to an AI-native app is a meaningful shift in product identity, and I think how AI layers into fintech tooling is one of the genuinely underexplored questions in the space right now.

Whether comparison-engine DNA helps or hurts here is a real question. More on that in a second.

The Micro: Twelve Years of Data and a Fresh Set of Clothes

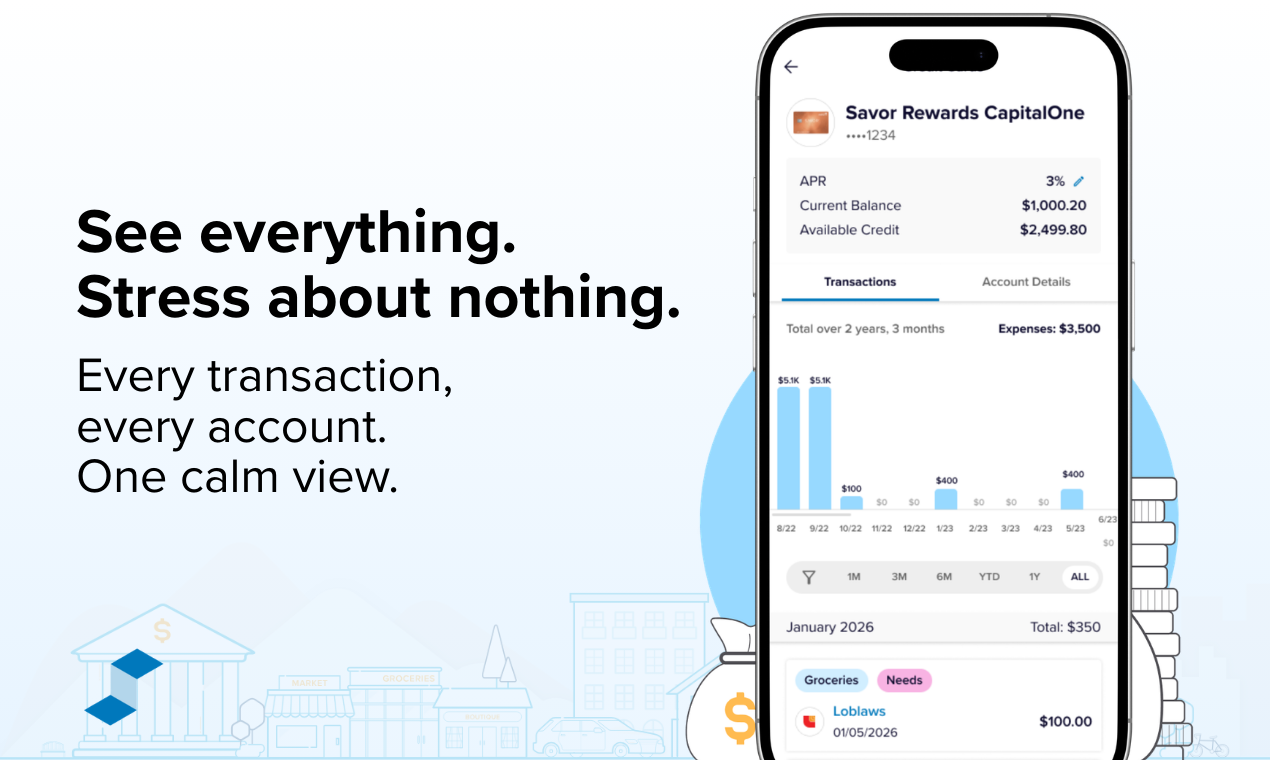

SuperMoney has been around since 2013 according to their own site, which means they have more user history and financial product data than most AI finance startups that launched in the last two years combined. They claim two million members. That’s not nothing. That’s actually a meaningful asset if the AI layer is built to use it.

The product positioning is action-first. Rather than showing you what you spent, it’s supposed to surface what you should do, optimize your debt, spot better financial products, flag if you’re off track. The tagline is “your money stress, solved by AI” and honestly I think the “financial calm” framing on the homepage is smarter than the tagline. Calm is something people will pay for. Stress reduction is a real emotional hook.

The Trustpilot score sits at 4.6 out of 5 based on 478 reviews, which is solid. User quotes on the site mention student loans, mortgage management, and ease of use, so the use cases are clearly broad rather than niche. One review specifically called out the comparison features helping with decision-making, which tracks with where the product came from.

When it launched (it got decent traction on Product Hunt, landing in the top five for the day), the comments were mostly curious rather than converted. People wanted to understand how the AI recommendations actually work, which is a fair question the site doesn’t fully answer.

The thing I keep coming back to is the business model tension. SuperMoney historically made money by connecting users with financial products, lenders, refinancing options. If the AI is recommending actions and some of those actions involve switching to a new loan product, is that a recommendation or a referral? Those are different things, and users know the difference. Something Viktor’s model of ambient AI assistance gets right is being explicit about what the tool’s incentives actually are. I’d want the same clarity here.

The Inc. 5000 five-years-running mention (according to a LinkedIn post from CEO Miron Lulic) suggests the underlying business has been healthy. That’s a better foundation than most.

The Verdict

I actually want this to work. The framing is right. The timing is right. AI personal finance that tells you what to do, rather than what you already did, is genuinely the product category that should exist.

But I have real questions. The comparison platform origin means there’s an inherent conflict between “we help you make the best financial decision” and “we get paid when you take a loan through our partner.” That conflict isn’t disqualifying, but it needs to be handled transparently or it will become the dominant narrative about the product.

At 30 days I’d want to see retention numbers on people who actually connected their accounts and came back. At 60 days I’d want to know whether the AI recommendations are generating real behavior change or just anxiety. At 90 days the question is whether the comparison revenue model and the AI advice model can coexist without one eating the other.

The two million member number is the real asset here. If Miron and the team can turn even a fraction of that existing base into active AI app users, they have something. Starting with an audience is a luxury most new fintech products don’t have.

I just need to know whose side the AI is actually on.

Also featured on HUGE: The Contract Amendment Problem Nobody Talks About Because Everyone Just Rereads the Whole Thing · Goldbridge Wants to Be Ramp for Landlords and I Think the Timing Is Right · FullSeam Wants to Replace Your Accounts Payable Team With AI Agents